On July 8th, Cleantech Group delivered a webinar, Readability By way of Chaos, revisiting the predictions we made initially of the 12 months relating to what is anticipated to develop, move (progress at a normal tempo with nuance), and gradual (face headwinds) in 2025. We took inventory of how the barometer has shifted in simply six brief months, and the place we see the needle transferring over the subsequent six, and past.

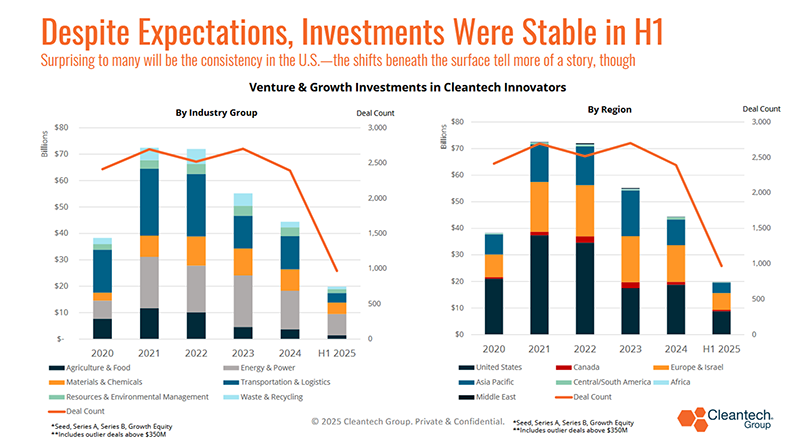

Opposite to expectations of a serious drop-off, investments within the first half of this 12 months are typically commensurate with the pattern seen final 12 months, significantly by way of know-how space breakdown, with a focus in Vitality & Energy. The U.S. has not skilled a serious drop-off in investments both.

Nevertheless, the high-level view doesn’t inform the entire story, and there are important variations between 2025 and former years taking place underneath the floor.

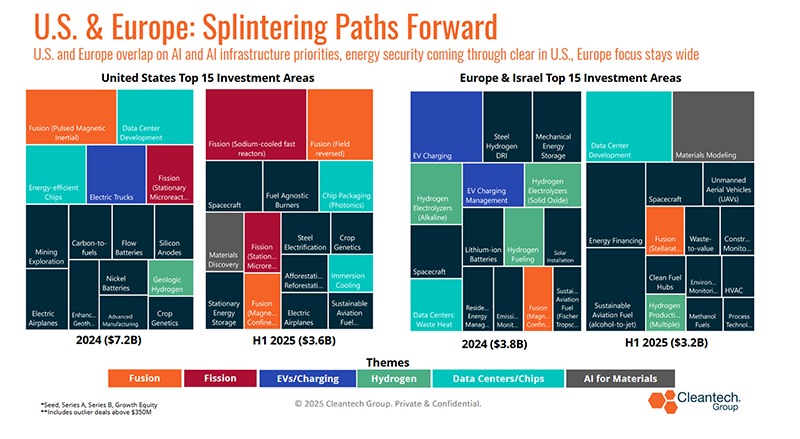

Within the U.S., the highest 15 funding areas present a powerful focus round themes of power safety and the AI revolution. These two areas very-much-so dovetail into one another, for instance, fusion and fission applied sciences assist the event of knowledge facilities and tackle considerations round power safety and independence. There may be additionally important exercise in information middle and compute effectivity.

In Europe, there’s some give attention to information facilities and future power sources; the focus shouldn’t be as pronounced as within the U.S., with Europe’s funding panorama being extra widespread. The slight drop in European numbers shouldn’t be a shock, and one thing we’re describing as “transatlantic ache.” Europe is clearly dealing with macroeconomic uncertainty, rate of interest volatility, and commerce tariffs, that are impacting the funding temper. Traders and firms are largely adopting a “wait and see” strategy, holding off on funding choices till there may be extra readability on rates of interest, commerce flows, and tariffs.

Each the U.S. and Europe have seen a drop-off in investments in electrical mobility and hydrogen from 2024 to 2025, at the very least for now.

Challenges in Elevating New Cash

It’s presently a problem to boost new cash for varied causes, together with institutional buyers (LPs) protecting money liquid attributable to uncertainty, making them unwilling to decide to new funds. Uncertainty round exit alternatives or attainable IPOs signifies that funds can not liquidate, and in consequence, LPs are extra reticent to reallocate capital.

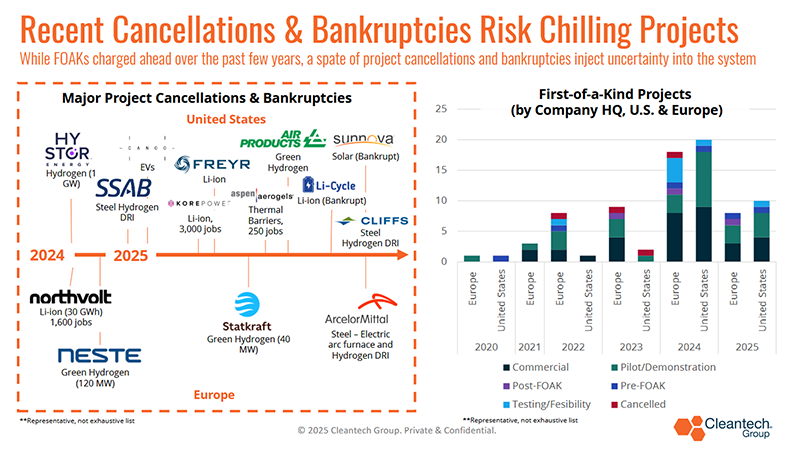

Nevertheless, investments solely ever inform a part of the story. Actual tasks and manufacturing are sometimes the strongest bellwethers of market readiness and receptivity towards clear applied sciences. It’s actual tasks and manufacturing which can be presenting the strongest challenges proper now.

Undertaking Cancellations and Bankruptcies

The previous 6-8 months have seen a spate of venture cancellations and bankruptcies, significantly within the U.S. This pattern shouldn’t be confined to at least one area however is seen throughout hydrogen, photo voltaic, battery manufacturing, and inexperienced metal. Within the U.S., large-scale manufacturing and tasks started to face financial realities initially of the 12 months, significantly because it’s more durable to execute a industrial facility for the primary time in comparison with merely elevating funds for demonstrations and pilots. That was even earlier than coverage alerts turned adverse for a lot of of those areas. And, whereas there’s a wholesome quantity of first-of-a-kind tasks being stood up, these had been seemingly in movement a 12 months or extra in the past, suggesting a possible lagging impact to come back.

Whereas Europe doesn’t have the identical stage of coverage uncertainty because the U.S., it continues to face very excessive power costs in comparison with the U.S. For some European venture cancellations, excessive power prices are a key explanatory issue, significantly for first-of-a-kind tasks the place it’s arduous to make industrial sense. That is particularly vital for sectors like inexperienced metal and hydrogen, the place it’s merely tough for Europe to compete attributable to these very excessive prices.

The Northvolt venture cancellations and subsequent chapter despatched “chilly alerts” and “rippling results” to the European finance sector relating to the prospects of scaling new manufacturing mega-projects. There’s a palpable threat averseness amongst buyers in comparison with a 12 months or two in the past. The market is extra discerning towards metrics round industrial viability and know-how readiness ranges (TRL) of tasks right now. As a consequence of budgetary constraints, there’ll seemingly be fewer European grants as effectively, with a higher give attention to de-risking instruments comparable to public ensures, counter-guarantees, and blended finance to maximise the effectivity of each Euro spent.

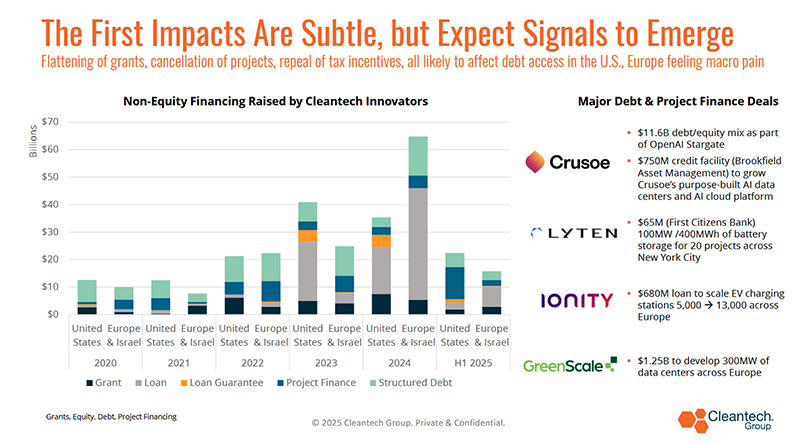

Non-Fairness Financing

When taking a look at non-equity financing, the U.S. drop-off from 2024 to 2025 doesn’t appear as important, but it surely’s essential to notice that over $11B of those figures are attributable to at least one main deal: Crusoe Vitality’s $11.6B take care of OpenAI’s Stargate venture.

Within the U.S., bankable themes on this area are largely centered round AI, which has a transparent demand pull regardless of coverage, whereas Europe’s focus areas are extra widespread, although the info facilities pattern can be current, e.g., GreenScale’s late ’24 mortgage to add 300MW of a deliberate 1GW information middle capability throughout Europe.

Past completely different sectoral focuses, Europe has a barely much less various capital stack for non-dilutive finance in comparison with the U.S. with roughly 80% of non-dilutive finance in Europe nonetheless supplied by banks, that are extremely regulated by way of the chance they will undertake. Banks usually have a distinct, probably extra conservative, urge for food for know-how threat, making them extra reticent to lend in an setting of excessive uncertainty. That’s compounded by a studying curve on the monetary aspect relating to supporting newer, much less acquainted applied sciences.

Again in January, I delivered our expectations for 2025 with Cleantech Group’s CEO, Richard Youngman, by 3 lenses: Develop, Move, and Sluggish.

The Develop Class: What’s Nonetheless Accelerating

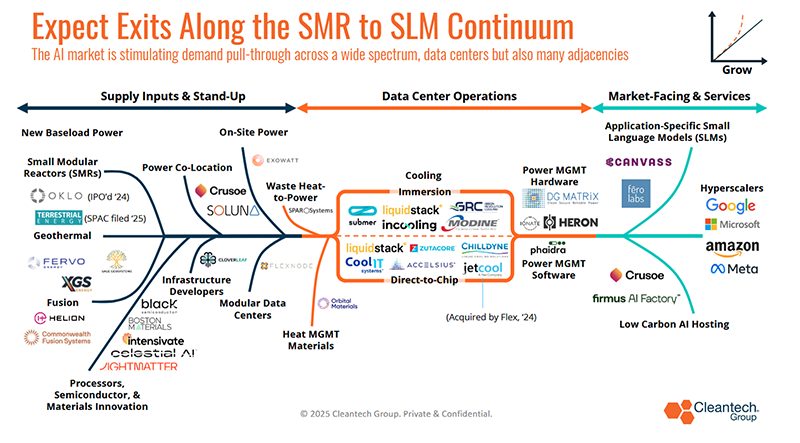

We Anticipate Continued Acceleration Alongside the AI Infrastructure Continuum

Of little shock is the demand for cleantech innovation stimulated by the AI revolution. This isn’t nearly information facilities; it’s a profound pull-through impact throughout your complete cleantech panorama. From new sources of baseload energy to superior supplies and semiconductors, and infrastructure growth round energy collocation, AI is driving demand.

We’re seeing intense exercise in areas like cooling and energy administration inside information facilities, in addition to providers designed to make compute much less power intensive. Whereas we predicted extra exits alongside this continuum, the sheer exercise and underlying demand are simple. Nonetheless, holding ourselves accountable for predictions: now we have solely seen one exit alongside this continuum this 12 months, that of Terrestrial Vitality, within the type of a Might ’25 SPAC announcement.

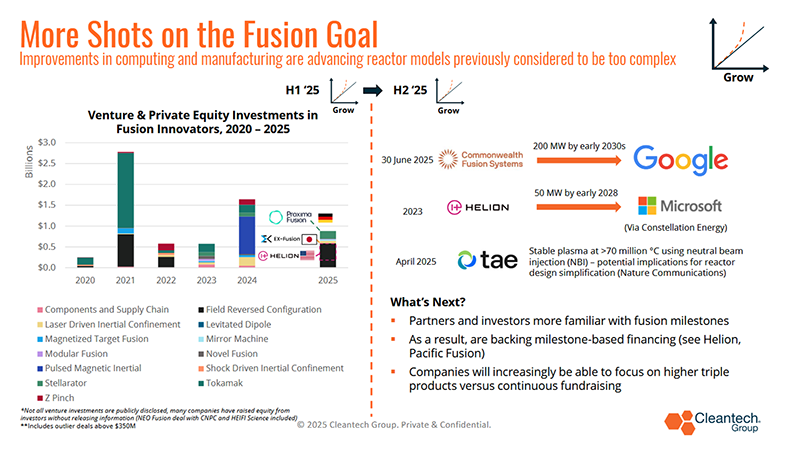

Fusion has gone from feeling distant to surprisingly near-term, with investments remaining important and geographically various, extending past the U.S. and Europe to Asia-Pacific. Extra impressively, we’re seeing industrial traction, such because the June ’25 500MW PPA between Commonwealth Fusion and Google, and an earlier one between Helion and Microsoft. The sheer quantity of technical breakthroughs up to now 5 years or so, exemplified by TAE Applied sciences’ April plasma breakthrough, has elevated consolation with the know-how as industrial offtakers and buyers grow to be extra conversant in fusion milestones. The range of reactor varieties (over a dozen) receiving consideration and funding additionally signifies rising familiarity and luxury with the longer growth timelines.

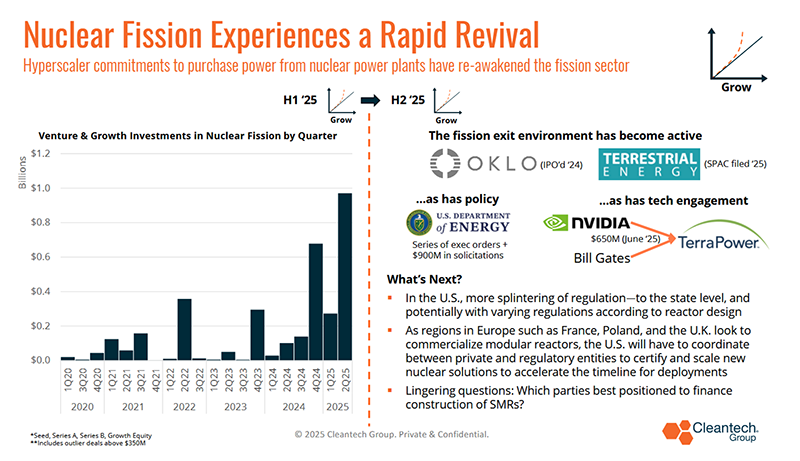

Nuclear fission had a really robust Q2, considerably boosted by the TerraPower deal which noticed participation from Nvidia and Invoice Gates. This area enjoys a uncommon energetic exit setting (e.g., Terrestrial Vitality’s SPAC submitting) and robust administrative assist within the U.S. We count on to see extra localized laws and tailor-made approaches to reactor varieties to ease growth. Whereas market forces are intensifying the urgency, lingering questions stay about who will finance development, as conventional PPAs are unlikely to account for all variables in allowing and setting up a fission reactor.

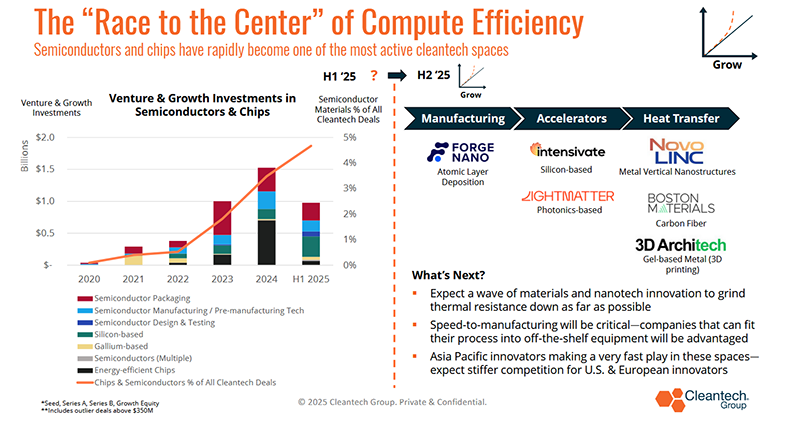

Compute effectivity is, in our opinion, one of the ignored shiny spots in cleantech proper now. The range of innovation throughout the worth chain is fascinating, from semiconductor manufacturing (e.g., Forge Nano) to {hardware} (e.g., Intensivate, Lightmatter, Celestial AI) and even warmth switch supplies on the nanotech stage (e.g., NovoLinc, Boston Supplies, and 3D Architech).

Given the growing power depth of chips, every thing alongside this worth chain will probably be vital. Velocity to manufacturing and scale is paramount right here – demand for these merchandise is near-term, and winners will want to have the ability to work with standard manufacturing approaches and gear. That is additionally a fiercely contested world area, with important innovation coming from Asia-Pacific, China (e.g., Semi-Tech), South Korea (e.g., DeepX), and Singapore (e.g., Silicon Field).

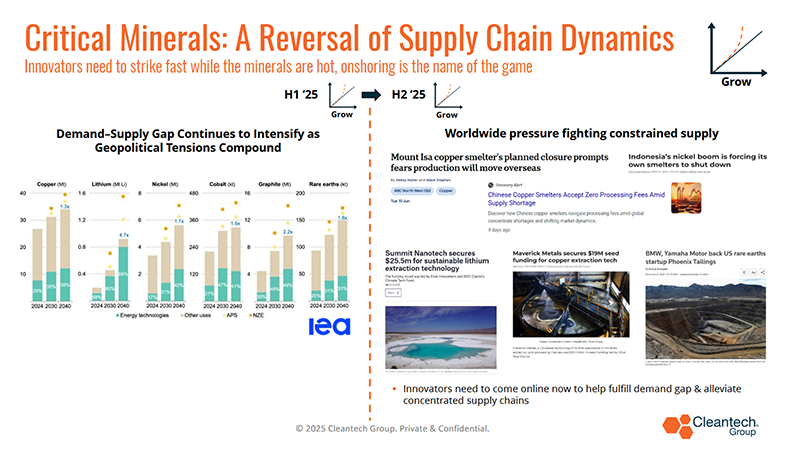

Vital Minerals

Vital supplies are foundational to all clear applied sciences, and the demand-supply hole is extremely intense. The IEA reported in Might on important future demand, projecting lithium demand to be nearly 5 instances what’s presently wanted by 2040, and a 30% enhance in copper demand. The mining sector alone requires $500-$800B in funding to fulfill these targets. The present provide chain dynamics are complicated, with mines holding energy, processors dealing with shortages, and smelters shutting down globally.

Whereas navigating China is an element, it’s not solely a commerce downside, nor will it’s solely a commerce answer. Innovators like Summit Nanotech (direct lithium extraction), Maverick Metals (copper, uncommon earths, lithium), and Phoenix Tailings (uncommon earth provide) are making important progress.

Provide Chain Dynamics: At present, mining holds energy, as processors face shortages of concentrates from mines and are even buying and selling at zero or adverse charges, keen to pay for provide. It is a world challenge, not only a China commerce downside, with smelters worldwide shutting down attributable to brief provide. Crucially, with mining permits taking 5-10 years, it’s “now or by no means” for brand spanking new improvements and mines. The lately handed One Huge Stunning Invoice (OBBB) removes the everlasting 45X superior manufacturing tax credit score for vital minerals manufacturing, as a substitute phasing it out after 2033.

Whereas the Overseas Entity of Concern (FEOC) restrictions put ahead within the OBBB will nudge producers to have interaction onshore extraction and refining, the shorter timeline on tax credit score availability probably dulls this nudge. It will undoubtedly elevate prices for U.S. home producers of vital minerals, who seemingly modeled mine lifetime with these credit in thoughts.

Even so, there may be observable drive by demand house owners to safe supplies domestically (see the latest MP Supplies offers with The Pentagon and Apple), indicating a willingness to pay value premiums for onshore supplies – a vital window of alternative for innovators. We additionally imagine that, given the brand new FEOC restrictions, there’s a potential second wind coming for e-waste recycling as a vital supply of supplies within the U.S.

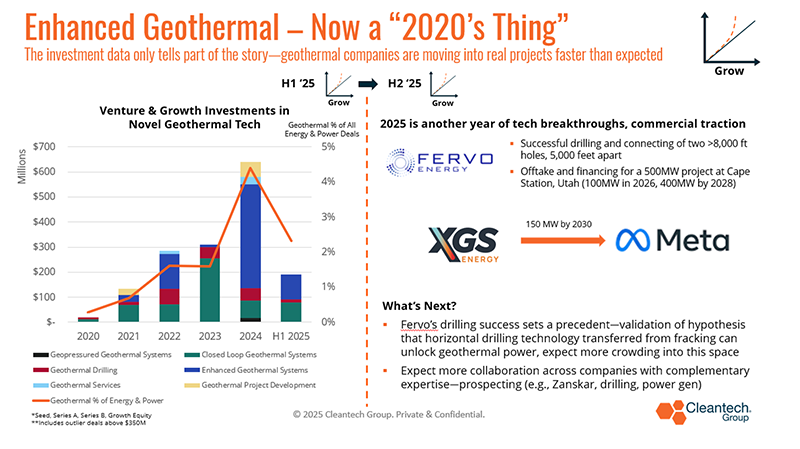

Enhanced Geothermal

Whereas investments inform a constructive story, the actual pleasure lies within the industrial traction and technical breakthroughs. We’ve seen extra promising industrial agreements together with Fervo Vitality securing off-take financing for a half-gigawatt facility in Utah and XGS partnering with Meta. Additional, the pull-through impact from the AI revolution and information middle energy wants has put know-how into the sphere sooner than anticipated, producing technical breakthroughs at a speedy charge.

Take Fervo’s outcomes over the previous 12 months or so, lately demonstrating drilling depths over 15,000 and accessing temperatures of 520°F, the Cape Station venture has reported a number of holes >8,000 ft. vertical, linked through a 5,000 ft. lateral gap to create a big “wine rack” formation. These developments are essential, as a result of they validate some key hypotheses round know-how switch from different industries – in Fervo’s case, horizontal drilling from pure gasoline fracking.

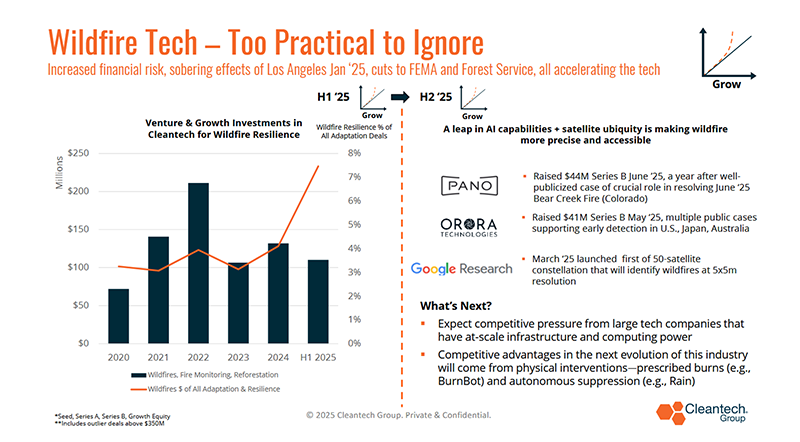

Wildfire Resilience

Sadly, this “develop” class is pushed by necessity. Investments are on monitor to outstrip final 12 months’s figures, and extra importantly, applied sciences are demonstrating real-world influence. Firms like Pano AI and OroraTech are publishing case research of fires they’ve helped mitigate – now in a position to level to demonstrable outcomes of harm averted. Curiously, massive tech gamers like Google are coming into the area with initiatives like Google Firesat, a 50-satellite constellation (the primary of which launched in March) for early wildfire identification – aggressive stress on innovators is more likely to enhance as AI incumbents proceed to start to see a receptive market.

We count on the proliferation of early identification applied sciences, boosted by latest jumps in AI capabilities to cut back prices of early response. Nonetheless, the chance imposed by wildfires (already estimated by MunichRe to have totaled $136B in 2015-2024, with solely $80B insured) is sufficient to require extra adoption of tech, and tech that performs at completely different phases of fires. We predict this to clean adoption prices for demand house owners and supply a lift for direct intervention applied sciences like prescribed burns (e.g., Burnbot) and autonomous suppression (e.g., Rain).

The Move Class – What Do We Anticipate to Proceed at Tempo?

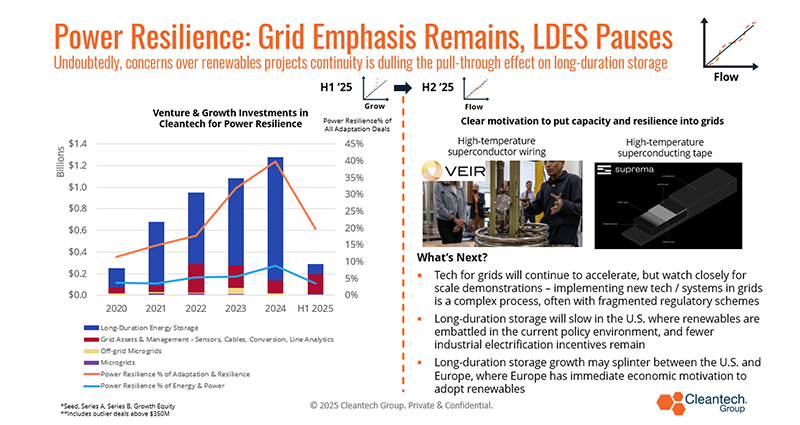

Energy Resilience

Probably with some controversy, we’ve moved this from “develop” to “move”, principally attributable to a blunted pull-through impact on long-duration power storage (LDES) from renewables within the U.S. and extra modest expectations for industrial decarbonization tasks off a spate of Workplace of Clear Vitality Demonstration venture cancellations. Whereas the LDES drop-off is well noticed within the fairness funding figures, there may be certainly some regional nuance.

Not like the U.S., Europe doesn’t have the native entry to grease and gasoline required to realize power independence with fossil fuels, and in consequence, power safety and renewables deployment are synonymous in some European circles, and conversations round sensible modifications comparable to allowing reforms for renewables are seen as power safety measures. Because of this, we count on LDES to proceed deployment in Europe to increase the effectiveness of renewables. Certainly, industrial developments (like Vitality Dome’s with Engie in Italy) and FOAK financing preparations (like Malta’s with BBVA for 14MWhe in Spain) are alerts that LDES is slowly edging into the mainstream in Europe.

The nuances are completely different round grid applied sciences, that are experiencing what’s more likely to be their strongest funding 12 months but in 2025. Generational electrical energy demand from the AI revolution, the necessity to handle unseen capability on grids, and surgically handle energy flows at websites of excessive financial worth (information facilities), is spurning curiosity throughout the grid tech spectrum. Applied sciences which have remained comparatively static for many years are hastily being re-invented and attracting quick curiosity.

Previously 12 months, we’ve seen a wave of Seed and Collection A rounds towards new kinds of transformers: DG Matrix ($20M), Heron Energy ($38M), and Ionate ($17M). There may be additionally palpable enthusiasm round high-temperature superconductors (HTS), each of their wiring incarnations (e.g., Veir) and in HTS parts (e.g., Suprema Tape). Watch the HTS parts area intently – HTS has promise not just for grid tech, but in addition for fusion reactors and energy-efficient chips. In a future the place fusion turns into attainable at a industrial scale, a part manufacturing race will ensue, with HTS parts turning into a linchpin know-how for growing price benefits.

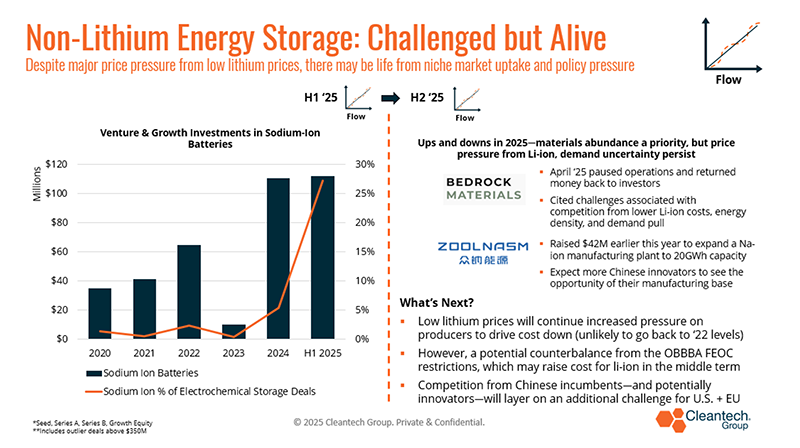

Non-Lithium Storage

This class stays in “move.” Whereas investments inform a typically constructive story, there are ups and downs, exemplified by Bedrock Supplies returning cash to buyers once they foresaw a probability that their sodium-ion batteries wouldn’t compete with lithium-ion at present lithium costs. A much-circulated paper in Nature earlier this 12 months highlighted the power density beneficial properties that sodium-ion would wish to make with a purpose to compete with lithium-ion.

Nevertheless, the OBBB’s important overseas entity of concern content material thresholds (60% non-FEOC in 2026, 85% by 2029) might present a second wind for sodium-ion and related applied sciences, as it will likely be difficult to supply compliant lithium batteries domestically if supplies largely originate from China. Even with that potential opening, count on continued competitors from China in sodium-ion, with incumbents like CATL and revolutionary start-ups like Zhongna Vitality energetic within the area.

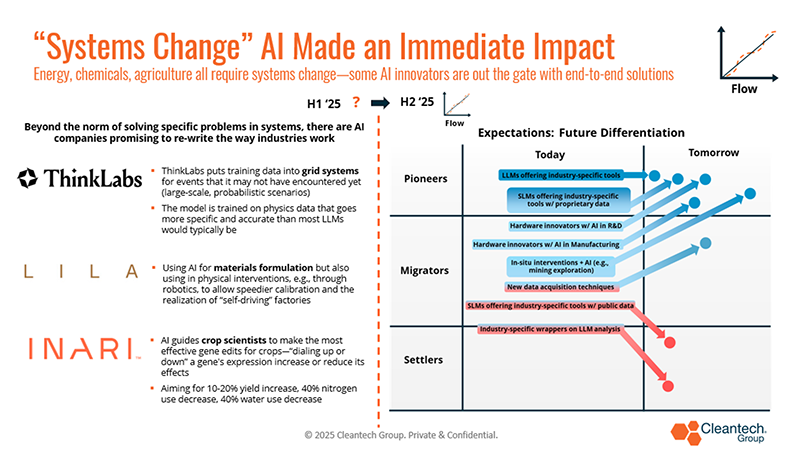

“Programs Change” AI

Whereas now we have noticed the influence of AI on cleantech – not simply software program, however {hardware} innovation, too – over the previous few years, a pattern we didn’t have categorized in January that we do now could be that of “programs change” AI. Programs change AI are options that we see as overhauling your complete means that sure programs work, versus options to particular issues or subsets.

Examples embrace:

- ThinkLabs: Create end-to-end grid modeling and administration utilizing physics-informed fashions, primarily offering “tens of hundreds {of electrical} engineers” to diagnose and resolve points within the grid. This will probably be an particularly essential answer as utilities must map enhancements to the grid to accommodate generational demand development at a time when grid liabilities attributable to pure catastrophe threat are growing.

_ - Utilities and ISOs are already seeing the worth in generative AI for grid administration and outage prevention; see the latest collaboration between CAISO and OATI’s Genie product. We count on extra of this within the coming months.

_ - Lila Sciences: Leverage AI for supplies formulation and direct interventions with robotics to create self-driving factories for battery supplies and hydrogen electrolyzers. This innovation represents greater than only a change to the science of supplies discovery, however a step change within the iteration course of to see which new supplies work and don’t work in the actual world, and far sooner.

_ - Inari: Makes use of AI to information crop scientists to exactly perceive and manipulate plant DNA. As a substitute of conventional, usually time-consuming breeding strategies, they will use AI-driven evaluation of in depth information units to pinpoint precisely which edits and edit varieties could have probably the most constructive impacts at particular areas inside a crop’s DNA construction.

_ - As now we have put ahead in latest months – AI could have a large influence on the event of crop inputs because of R&D effectivity beneficial properties at a time when altering climate patterns are closing the home windows of alternative to regulate crop therapies however opening the door to improvements like biostimulants to enhance up to date approaches.

With that stated, not each AI cleantech firm will succeed. We see a transparent differentiator for firms providing industry-specific instruments with proprietary information, fairly than these counting on public information or LLMs, which can grow to be commoditized. AI integration in R&D, manufacturing, and in-situ interventions (like mining) will present important aggressive benefits. One other solution to say it – AI would require an information uniqueness benefit, deep tech integration, or each, to proceed standing out throughout the cleantech theme.

The Sluggish Class – What Will Proceed to Face Headwinds?

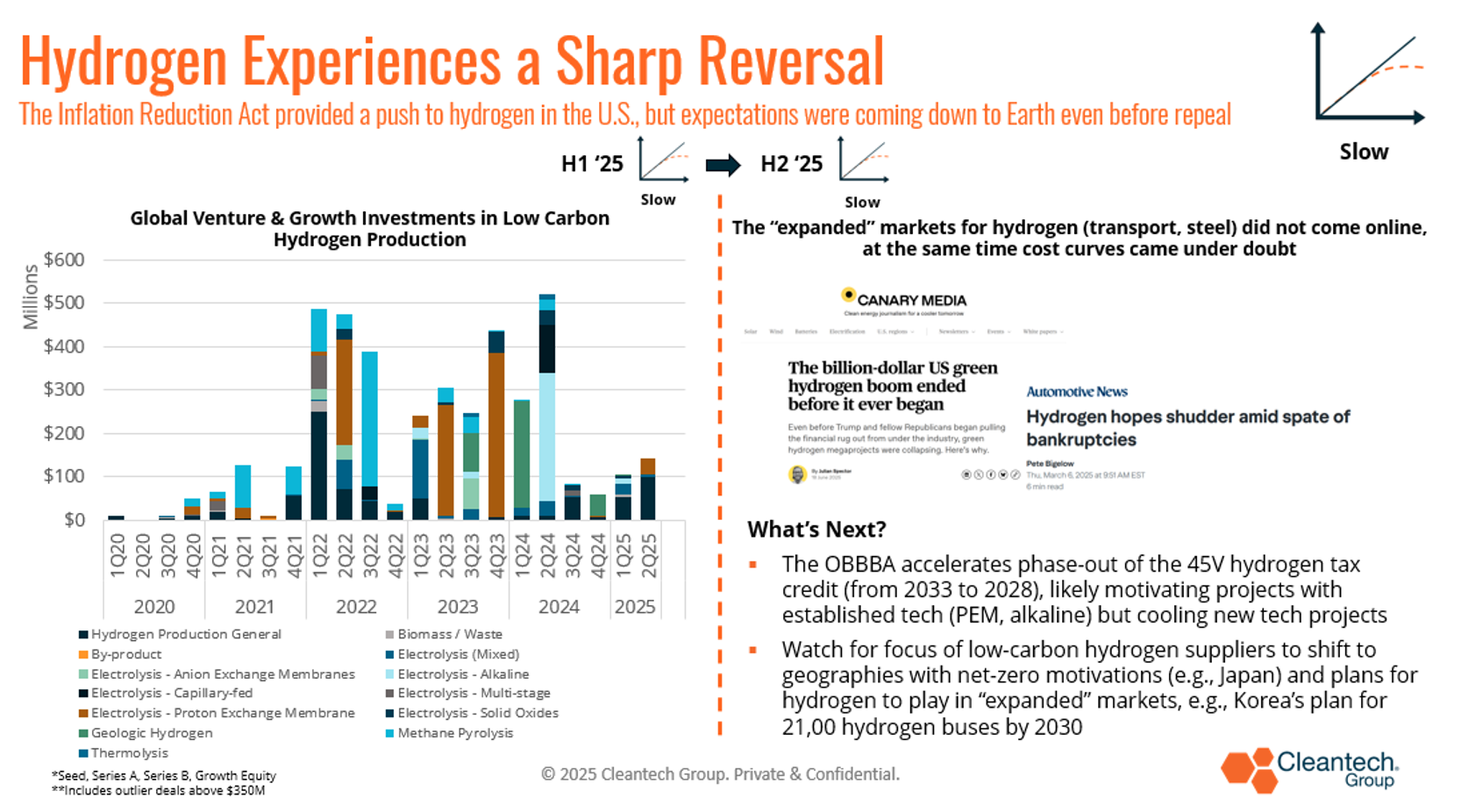

Hydrogen

This stays firmly in our “gradual” class. The elemental dynamic hasn’t modified: adoption markets exterior of conventional makes use of like sure chemical substances and ammonia-based fertilizers haven’t picked up. We’ve seen quite a few cancellations of hydrogen-based inexperienced metal tasks in latest months and the extra hypotheses like distance transport haven’t borne out.

The OBBB’s accelerated phase-out of the 45V hydrogen tax credit score (from 2033 to 2028), whereas not eliminating it, will make it more durable for brand spanking new hydrogen manufacturing applied sciences to get off the bottom in time to take benefit. There’s a regional nuance right here, with some hydrogen innovators shifting focus to Asia-Pacific, significantly Japan and Korea, the place important authorities targets and adoption momentum exist. An instance is Amogy’s July 15th announcement that it accomplished $23M of its latest $80M fundraise spherical to give attention to bringing ammonia-to-power (maritime, stationary storage) to APAC international locations together with Japan, Korea, and Singapore.

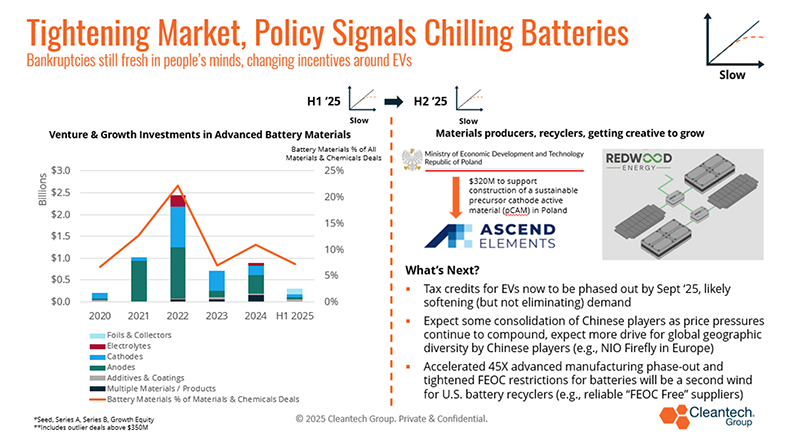

Battery Manufacturing and Supplies

Within the U.S., the accelerated phase-out of electrical car (EV) tax credit in September 2025 will boring (however not get rid of) demand for EVs, and thus gradual the market pull-through for EV batteries. As put ahead in our year-ahead outlook in January, main world venture cancellations (e.g., Kore Energy and FREYR Battery) and bankruptcies (e.g., Northvolt) have introduced into sharp focus the challenges of vertically-integrated battery manufacturing within the U.S. and Europe.

Nevertheless, some innovators are discovering artistic options, comparable to Ascend Components leveraging European alternatives or Redwood Vitality repurposing second-life batteries for information middle backup storage. Furthermore, the FEOC restrictions for battery manufacturing referenced earlier are more likely to problem producers of batteries which can be sourcing Li-ion supplies and parts from China (the bulk). An attention-grabbing byproduct of this growth could also be a second wind to battery recyclers within the U.S. This will appear counterintuitive, given the latest Li-Cycle chapter, however with the brand new FEOC restrictions set to use to manufacturing amenities established submit 2025, supplies recyclers that may effectively entry feedstock could also be in place to offer “FEOC-free” battery supplies.

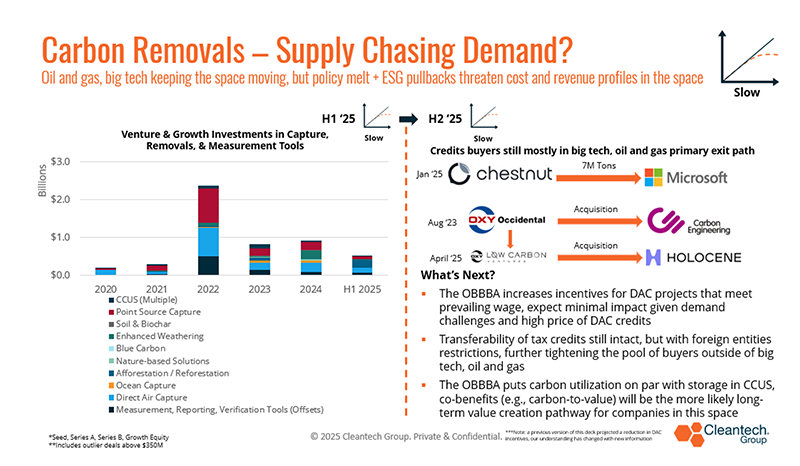

Carbon Removals

Carbon removals stay within the “gradual” class regardless of respectable funding and industrial traction. The belief points we mentioned on the outset of the 12 months round voluntary carbon market’s “phantom credit” and associated controversies nonetheless linger, and at a time when company commitments are receding. The pool of consumers for credit and acquirers of firms stays extremely concentrated in massive tech and oil and gasoline, and there are solely so many of those consumers to go round.

Microsoft’s latest deal with Chestnut and Oxy Low Carbon Ventures’ latest acquisition of Holocene (word that Occidental Petroleum additionally acquired Carbon Engineering in 2023) are proof of the place momentum comes from on this area. The OBBB, whereas permitting tax credit score transferability, has tightened restrictions on overseas entities shopping for credit, additional shrinking the market.

Nevertheless, there may be now extra potential for the utilization sections of the carbon seize, utilization, and storage (CCUS) to develop because the OBBB now locations CCUS on the same footing for tax credit, encouraging co-benefits like carbon-to-value and carbon-to-fuels. On the sustainable aviation fuels (SAF) entrance, the OBBB does scale back the part 45Z manufacturing tax credit score quantity ($1.75/gallon to $1/gallon) however extends credit by two years by 2029. So whereas we count on the carbon removals market to stay challenged, we count on SAFs that use carbon as an enter (e.g., e-SAF) to proceed growing at present momentum. See progress on tasks like Infinium’s Undertaking Roadrunner as indicators.

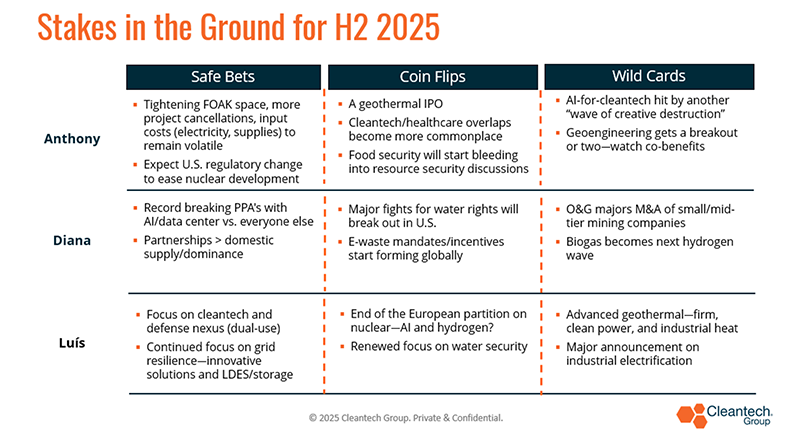

Our H2 2025 “Bingo Card”

We divide this part into “Secure Bets,” “Coin Flips,” and “Wild Playing cards.” In every space, my colleagues and I gives you our daring predictions.

Secure Bets – Issues We Really feel are Prone to Happen

Anthony DeOrsey, Analysis Supervisor

-

- The Overseas Entity of Concern (FOEC) coverage is anticipated to tighten, making manufacturing and constructing tougher attributable to coverage, tariffs, and rising electrical energy costs.

- There may even be extra regulatory modifications on the native/state stage to ease nuclear (fission) growth, tailor-made to reactor varieties, to draw financial exercise pushed by information facilities and AI.

Diana Rasner, Group Lead, Materials & Chemical compounds and Waste & Recycling

Diana Rasner, Group Lead, Materials & Chemical compounds and Waste & Recycling

-

- AI-driven information middle PPAs (energy buy agreements) will scale from megawatts to gigawatts.

- To handle vital minerals provide chain points, there will probably be extra partnerships growing throughout geographies and firms, fairly than a single home provide dominance, as a result of complexity and lengthy timelines for mining and manufacturing.

Luis Rebelo, Coverage Supervisor, Cleantech for Europe & Cleantech for Iberia

Luis Rebelo, Coverage Supervisor, Cleantech for Europe & Cleantech for Iberia

-

- Anticipate cleantech to merge with protection tech in Europe, creating dual-use functions, pushed by institutional capital deployment in protection and elevated public budgets.

_ - Grid safety and resilience may even be a secure guess, as latest blackouts in Spain, Portugal, the Czech Republic, and Italy spotlight the grid’s stress, resulting in extra give attention to revolutionary options and lengthy period power storage.

- Anticipate cleantech to merge with protection tech in Europe, creating dual-use functions, pushed by institutional capital deployment in protection and elevated public budgets.

Coin Flips – Issues We expect are Potential, However Might Go Both Manner in 2H 2025

-

-

A geothermal IPO is probably going before anticipated, pushed by sustained demand from the AI revolution and the precedence of power safety/independence, mixed with industrial traction and technical breakthroughs.

-

Cleantech and healthcare overlaps will grow to be extra obvious, with pharmaceutical innovators touting power use discount of their merchandise, probably main them to be acknowledged as cleantech innovators.

-

Meals safety will speed up into mainstream dialog, given its shut ties to power and nationwide safety, with elevated give attention to crop genetics.

-

-

- A much less heated debate round nuclear power in Europe is feasible, pushed by the EU’s want for low-carbon power for the AI race and the potential use of extra nuclear capability for pink hydrogen.

-

Water safety will return excessive on Europe’s agenda attributable to droughts, dry years, and rainfall shortages, with AI and information facilities including to the stress, particularly in Southern Europe.

Wild Playing cards – Issues We Suppose are Additional Afield, However Might Shock Us in H2

-

-

AI for cleantech might face one other wave of “artistic destruction”; whereas not a bubble, the quickly accelerating capabilities of fashions imply that firms counting on LLMs or public information will probably be challenged by newer, extra highly effective innovators.

-

A geoengineering breakout is feasible, significantly the place co-benefits exist, particularly when overlapping with the water and meals safety arguments, i.e., fashions that evolve from local weather arguments to useful resource safety arguments.

-

-

- A serious oil and gasoline or service firm would possibly interact in M&A with small-/mid-tier mining firms, leveraging their drilling and useful resource extraction experience (e.g., ExxonMobil in lithium extraction).

-

Biogas might grow to be the “subsequent hydrogen wave,” providing power resilience and provide, however with its personal set of challenges relying on regional benefits.

-

-

The function of geothermal power in Europe might considerably develop attributable to excessive power prices and the necessity for various electrification options, particularly with a brand new EU geothermal motion plan introduced.

-

There may be constructive surprises in industrial electrification bulletins in Europe, constructing on PPAs and behind-the-meter renewables/batteries, to counter the stagnation in Europe’s electrification charge.

-

How did we do? What would possibly we be lacking? And extra importantly, what are you seeing on the market?

{kind=link}